Our experts explain why volatility is making a comeback and how to get your portfolio ready for more ups and downs.

by Russ Koesterich, Portfolio Manager, Blackrock

As my team and I conduct our 2015 macroeconomic outlook meetings, we have made a conscientious effort to drive this message home: volatility is likely to resurface as the Federal Reserve (Fed) gets closer to adjusting its monetary policy stance, even if that adjustment is a measured affair. While it should not be a reason to exit the stock market entirely, investors ought to be more thoughtful in their asset allocation.

One direction no more. Despite some short-term hiccups in this six-year-long bull market, stocks have enjoyed a relatively stable upward ride, in what one could easily characterize as a one directional trade. Since the onset of the financial crisis, the Fed’s unconventional monetary policy has inadvertently suppressed volatility, encouraging market participants to hold more risk assets across equity and fixed income. But as the Fed removes its support, markets are likely to return to some normal ups and downs.

The curious notion that good news is bad news, and vice versa, doesn’t help calm the markets either. Case in point, the February U.S. employment report showing 295,000 new jobs is in and of itself stellar, but it seemed to confirm fears for some that the Fed would move to raise interest rates sooner rather than later. Stocks tumbled -1.42% as a result on March 6. By contrast, U.S. retail sales fell three months in a row, yet stocks rallied 1.26% after its February report release on March 12. We think the good news/bad news dynamics will get worse as the Fed rate hike draws closer. Watch out for a greater amplification of this volatility.

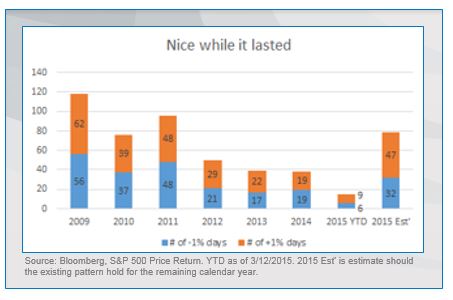

Nice while it lasted. Going back six years, we counted the days when the S&P 500 moved greater or less than 1% (see the chart below), and the result was quite telling. The market has steadied in recent years, evidenced by markedly fewer days of significant fluctuations. That said, volatility has been on the rise, a volatility spike thus far in 2015 suggests a volatile year to come. Projecting ahead, if the current pattern continues, 2015 would be the third most volatile year since 2009 for the S&P 500. Moreover, if we focus on down days (-1%) only, we would have to go back to 2011 to find a year with more down days.1

An end to bull market? Not necessarily, but it does mean the structure of the bull market is changing, and it’s a good time to think about what geographies or sectors could lead the next leg of this bull market. International stocks are rising with the backing of quantitative easing programs, with European and Japanese stocks up 18.4% and 9.1% year-to-date.2 In sharp contrast: U.S. stocks returned 2.3%.2 We think more moderate returns are likely in the cards for U.S. stocks this year, which makes a good case for international diversification.

Additionally, as volatility rises, investors should consider complementing momentum strategies with other risk factor segments such as quality or value. A rethink on bond proxies including utilities and REITs should also be in order because of these defensive sectors’ sensitivity to changing monetary conditions and the prospect of higher rates. We think cyclical sectors could weather the change better.

Taken together, markets will probably see more peaks and valleys this year, but for investors with a long time horizon, remaining invested pays off.

Sources:

1Past performance is not indicative of future results. The estimate is provided to illustrate the potential for a year end result based off an assumed path.

2Bloomberg. Price return as of 3/12/2015. European equities are represented by Euro Stoxx 600, Japanese equities by Nikkei 225 and U.S. equities by S&P 500. All returns are denominated in local currency.

Russ Koesterich, CFA, is the Chief Investment Strategist for BlackRock. He is a regular contributor to The Blog and you can find more of his posts here.

Terry Simpson, CFA, is a Global Investment Strategist for BlackRock. He contributed to this article.

This material represents an assessment of the market environment as of the date indicated and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any security in particular.

The strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. There is no guarantee that any strategies discussed will be effective.

©2015 BlackRock, Inc. All rights reserved. iSHARES and BLACKROCK are registered trademarks of BlackRock, Inc., or its subsidiaries. All other marks are the property of their respective owners.

iS-15172