by Erik Swarts, Market Anthropology

Although we would never dispute that markets often pivot on external catalysts, as we noted recently (see Here) - they often are just instigators of larger forces at play. For every time that a market perceives to be largely driven by breaking news or geopolitical events, we could reference fifty other occasions in which a similar development had no material influence.

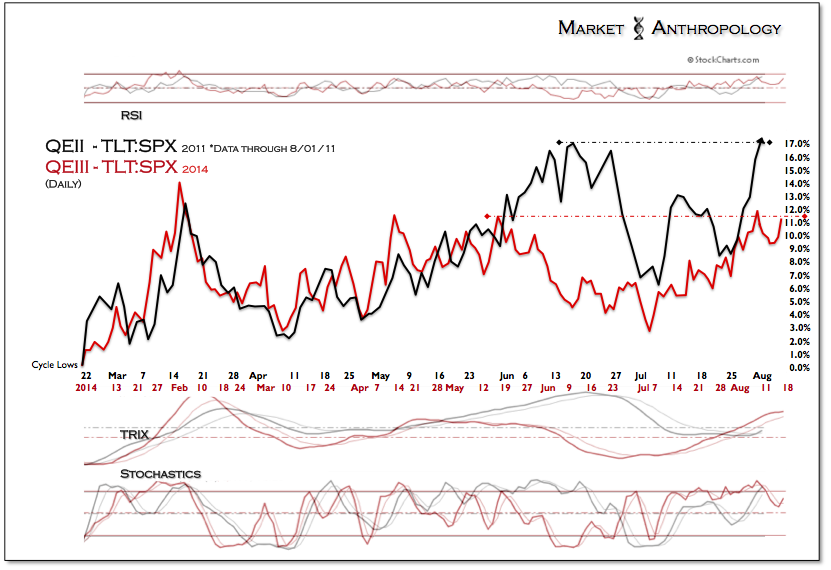

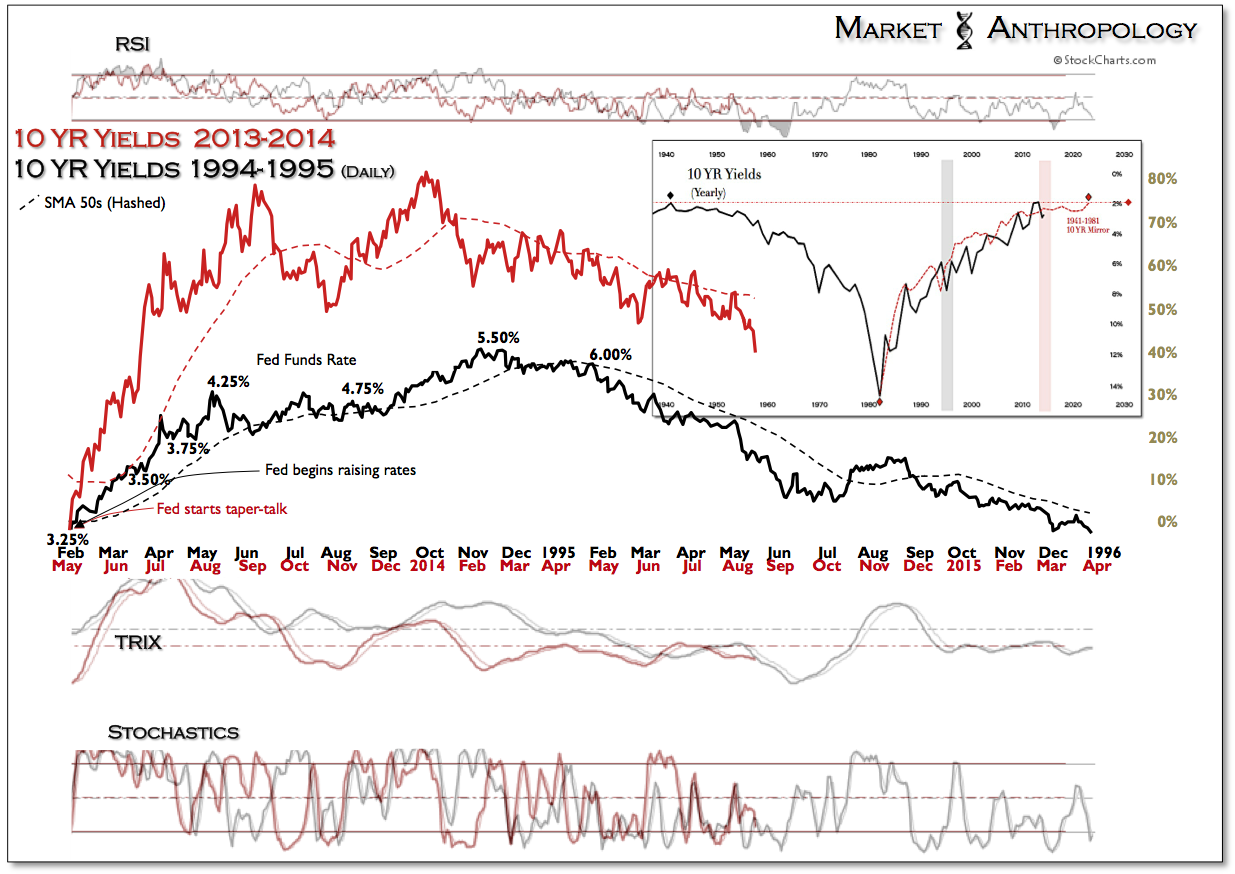

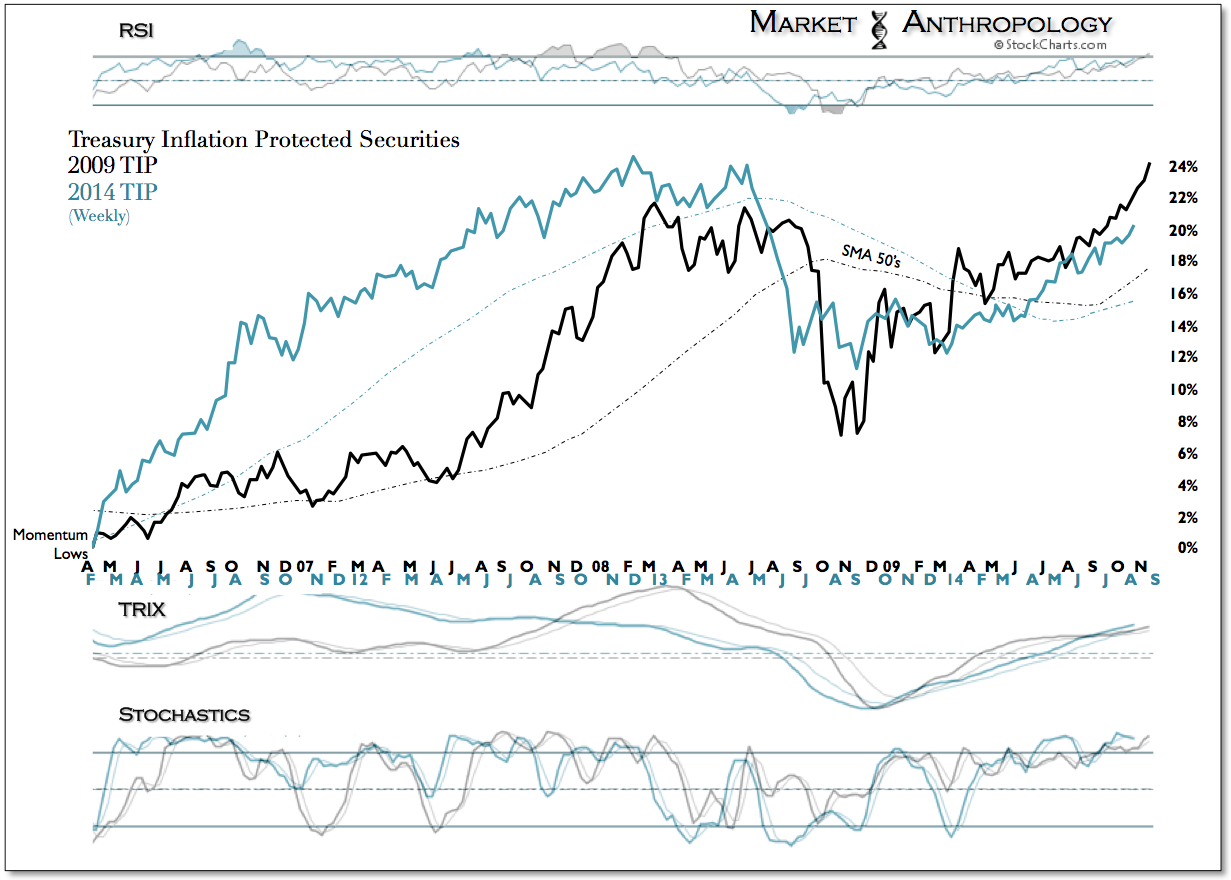

From our perspective, yesterday was a perfect example in which an exogenous event in Ukraine, motivated pre-existing conditions in the Treasury markets. Based on our comparative analysis of 10-year yields developed months before (see Here), the current breakdown truly comes as no surprise. In fact - it arrived right on schedule.

Should yields continue to breakdown further with equities next week, we can guess the nature of what the headlines might read. That being said, we continue to believe there are larger forces at play, just as there were in 2011 as the Fed first attempted to wind down QE - and in the mid 1940's when the Fed ended their extraordinary support of the Treasury markets.