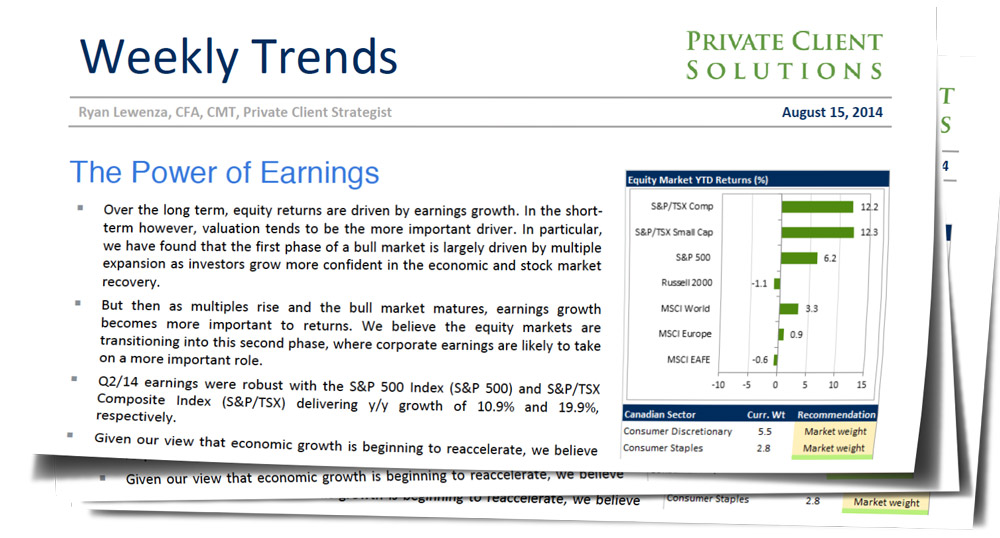

In Loving Memory of Dear Great Aunt Addy

by Guy Haselmann, Director, Capital Markets Strategy, Scotiabank GBM

· Hear ye, hear ye, Fed policy is hereby bestowed the name “Great Addy Policy” in memory of my great aunt who drove with one foot on the accelerator and one foot on the brake. This is fitting since the FOMC is physically applying the brake by ending its asset purchase program in October, while simultaneously blowing hot air into the accelerator in the form of promises of continued accommodation.

· Aunt Addy was unaware that operating the car in this manner would cause long run damage. Had she known, she may not have cared: the car moved forward, while it was being held back. At that current moment, she felt safer due to her misguided belief that she had greater control of the car.

· For those who went along for the ride on trips to the ice cream shop, it was a terrifying and high-stakes adventure. Witnesses (the adults who stayed home) deemed her effort to get to the destination, heroic. However, everyone knew that over time the ‘game of chicken’ dangers grew ever-greater.

· “Great Addy Policy” will be evident this week. The Fed Minutes on Wednesday will likely read a tad hawkishly, while Yellen’s Jackson Hole speech on Friday morning will likely provide more dovish pleonastic gobbledygook bunkum.

· The Fed Minutes could read a tad hawkish, because economic data going into the July FOMC meeting had been improving, and also because Charles Plosser dissented. He felt including the words “considerable period” was inappropriate because “such language is time dependent and does not reflect the considerable economic progress that has been made toward the Committee’s goals”. Moreover, although Richard Fisher did not dissent, he likely advanced and broadened Plosser’s line of reasoning.

· Yellen’s speech on Friday will likely discuss labor slack as a justification for uber-accommodation. It will be evident that Yellen is a Tobin Keynesian and Galbraith interventionist. She’ll sound professorial and academic, but for Fed critics it will do little to help them understand the logic behind the recent-year extraordinary actions of the FOMC.

· Critics will continue to point to the time-inconsistency (see June 25 Commentary) underlying their actions. Specifically, there are trade-offs whereby slightly more growth and employment today gets exchanged for significantly greater instability and higher unemployment later.

· The FOMC has used experimental tools for so long to keep the accelerator pressed that it fears what happens when the car stops. Therefore, the FOMC believes they have little choice other than to keep the car going forward, which works until it doesn’t. The risk/reward trade-off continues to skew unfavorably. The farther markets move into the right-tail side of the distribution curve, the deeper they will eventually more into the left-tail. Vrooom……Crash.

· The Galbraith-esque Fed believes it knows best. It believes that it has the authority to keep spiking the punchbowl and that it has the knowledge to know when and how to intervene in financial markets. It was easier for Aunt Addy to trudge down the highway at a steady pace than it was for her to make turns or park the car.

· Details of the Fed’s exit strategy loom in coming months. This week may offer a glimpse of the Fed’s stop-and-start journey; one that is peppered with bouts of confidence and the fear of not arriving at the proper destination fully intact - or at all.

· “Beware; for I am fearless and therefore powerful” – Mary Shelley

Read/Download complete report below: