Another Complementary Factor Modef

by Cam Hui, Humble Student of the Markets

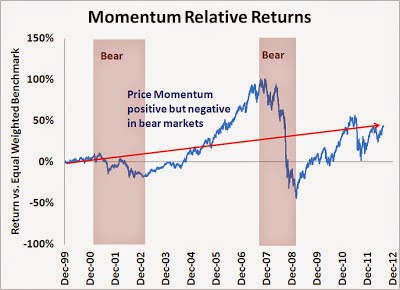

In the past, I had written about how combining factors can lead to more performance stability (see Momentum + Bull market = Chocolate + Peanut butter?). My past research showed that while price momentum did exhibit positive alpha over the course of a market cycle, returns were highly volatile.

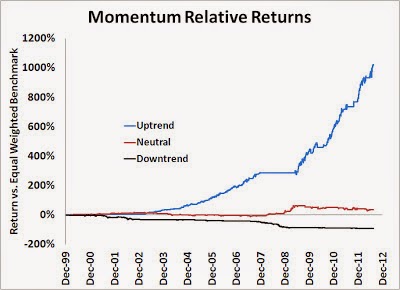

Instead, the Cass Business School paper entitled The Trend is Our Friend: Risk Parity, Momentum and Trend Following in Global Asset Allocation indicated that momentum worked much better when conditioned on bull and bear market cycles. The paper showed that returns to price momentum was especially positive during bull phases at a stock level. My research showed that this effect was extended to the sector and industry level. I identified bull (uptrend), bear (downtrend) and neutral market phases using a 50-200 day crossing moving average trend following system.

Quality and Value

Now comes some interesting research results from Research Affiliates showing conditioning value investing with certain quality factors potentially adds alpha as well (emphasis added):

We used three measures to capture the pertinent information: return on equity (ROE) to reflect growth and profitability; the debt coverage ratio to represent the likelihood of default; and the accruals-to-average-total-assets measure defined by Sloan (1996) to quantify possible accounting red flags.12 To arrive at company-specific quality measures, we used the simple arithmetic average of each stock’s percentile rank for these three variables.

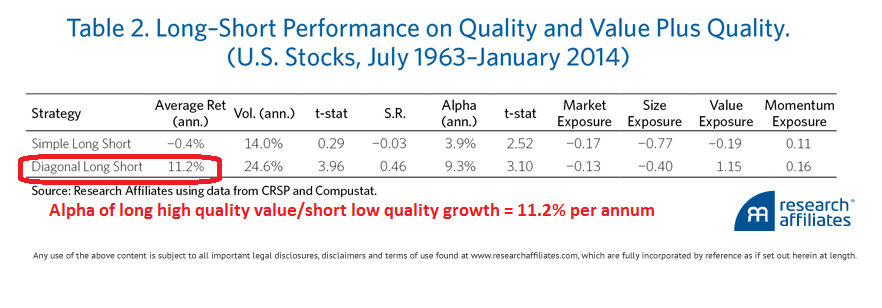

The first line of Table 2 shows the performance of a simple long–short strategy based on this quality measure. On average the strategy produces a small negative return. It has some alpha after we control for factor exposure and negative exposure to the value factor.

When we use quality in conjunction with value, the results are much better. The second line of Table 2 shows the results of a portfolio where we go long value stocks with high quality and short growth stocks with low quality. This long–short strategy has annual alpha of 11.2% per annum. A substantial portion of this statistically significant alpha comes from conditioning on quality information. The annualized alpha, controlling for the Fama–French–Asness–Carhart four factor model, is 9.3% per annum.

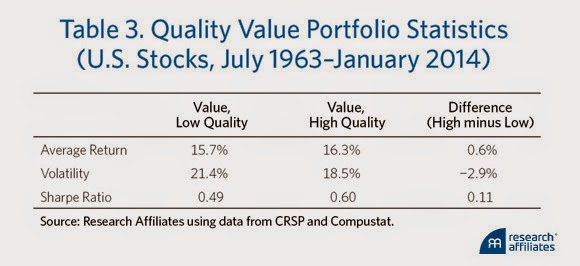

On a long-only basis, the value-high quality combination exhibited higher returns with lower volatility when compared to the value-low quality combination.

The authors concluded (emphasis added):

The high quality value portfolio has fewer distressed, slow growing, unprofitable companies with potentially questionable accounting practices. As a result, the high-quality value portfolio has a better risk-adjusted return. Quality is not, in itself, a factor that generates a premium; but value investing conditioned on a properly specified concept of quality is a powerful investment strategy.

This is another example of how combining factors can add value. In fact, the use of both of these disciplines, namely price momentum-trend following and quality-value, can be highly complementary strategies in a quantitative equity portfolio.

Copyright © Humble Student of the Markets