by Cullen Roche, Pragmatic Capitalist

I stirred up a little controversy in a recent post when I asserted that indicators like Tobin’s Q and Shiller’s CAPE might lead investors astray at times. In fact, I think there’s empirical evidence that this has happened at times during the last 20 years and particularly during the most recent 5 year bull market when valuations have been historically high according to these metrics. But I want to discuss something a little different – the concept of “value”.

In the previous post I asserted that “value” is a nebulous concept much like “beauty”. The reason it is nebulous is because none of us really knows what it is at any given time. And our concept of “value” is clearly dynamic. It is not a static concept. Therefore, applying a past period’s concept of “value” does not necessarily reflect what the current market might perceive. For instance, there have been times in human history when being overweight was deemed beautiful. But today when we are told what beauty is we are often showered with pictures of (grossly) underweight people. In fact, if you look at different cultures today you’ll find very different ideas of “beauty”. It’s obviously a dynamic concept that has no static historical benchmark.

The point is that the concept of “value” must be dynamic. It evolves and adapts just as we do. It is not a static concept that has some sort of eternal benchmark. Therefore, relying on past historical data is not necessarily a valid way of trying to “value” the current market. Indeed, John Templeton was wrong – this time is ALWAYS different because the current market and economic environment is its own unique set of circumstances with its own set of unique participants.

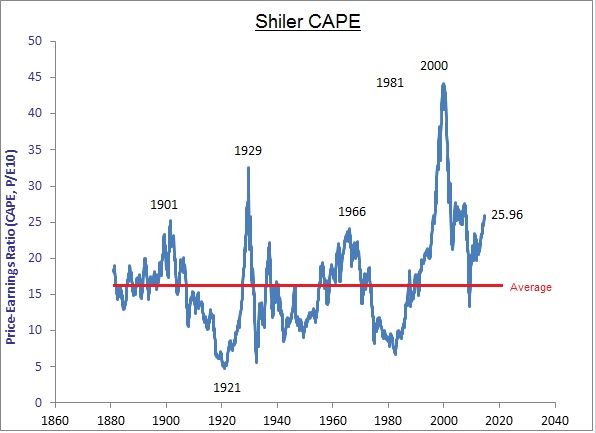

Now, this isn’t some permabull argument so please don’t take it that way. In fact, it could be taken as a permabear argument depending on your view. For instance, in the current market environment the Shiller CAPE is at roughly 26. That’s very high by historical standards when compared to the average of 16.5:

But what does that mean? In a historical sense it might mean that the stock market is very expensive and you should be underweight stocks. But what if this has no historical pertinence at all? What if US stocks are simply more “valuable” because global shares are that much worse? Or what if the share count of US corporations in public markets has been reduced to the point where demand is simply creating a new normal? Or what if perceptions have simply changed for no good reason at all and the average Shiller CAPE of 25.25 since 1990 is simply the “new” 16.5? We have no way of knowing any of these things because our own perception of “value” is dynamic and none of us know what the true measure of “value” actually is.

In short, these sort of metrics might have no statistical bearing at all on the current market environment. And in fact, the current “values”, taken in a historical sense, don’t mean that we can’t see severely negative and permanently depressed values in the future. After all, if I am right and “value” is a nebulous and dynamic concept then there’s nothing stopping the exact opposite of the current “overvalued” environment from persisting at some point in the future. And that environment, just like the current environment, will be its own unique set of circumstances with its own unique set of participants with no necessary dependency on the way “value” was perceived by past participants.

Copyright © Pragmatic Capitalist