“Short-term crashes can be painful, but long-term returns are far more important to wealth creation and destruction.” – Cliff Asness

Deep Risk was my favorite of the William Bernstein trilogy of Investing for Adullts series of Kindle books.

He sets out to show how investors should think about the stock market and comes up with a couple of working definitions for the actual risk we face as investors.

Risk can be defined in a number of ways in the world of finance (volatility, beta, Sharpe Ratio, Value at Risk, etc.) but Bernstein really drills down into the scariest part of investing in stocks for individual investors — losses.

He explains the difference between short-term and long-term risks:

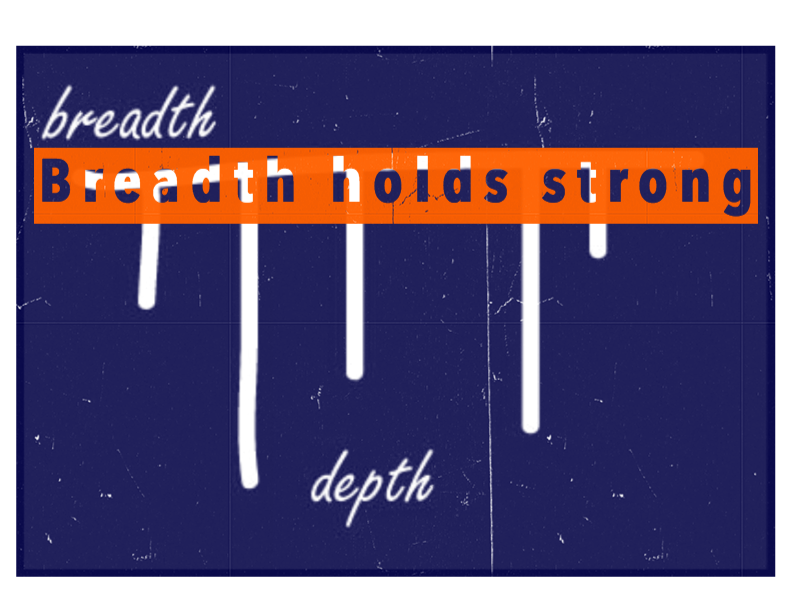

Risk, then, comes in two flavors: “shallow risk,” a loss of real capital that recovers relatively quickly, say within several years; and “deep risk,” a permanent loss of real capital.

This is important because one of the first things nervous investors say when they witness a stock market crash is, “I just want out of the market because I can’t stand to see anymore losses.”

This happened to many people during the financial crisis. And those that sold felt good about that decision at the time as stocks continued to fall.

That is, until the bleeding stopped and things turned around.

What these I’ll-buy-back-in-when-things-look-better investors fail to realize is that there’s never going to be a perfect time or gut feeling that will get you back into the market.

There will always be justifiable reasons to stay in cash just a little bit longer.

Bernstein goes even further by making the distinction between the two types of risk:

Put into different words, shallow risk, if handled properly, deprives you only of sleep for a while; deep risk deprives you of sustenance.

Shallow risk is simply the fact that stocks go down from time to time. Get used to it. Stocks make you money in the long-term because they can lose you money in the short-term.

Shallow risk happens quite often.

More from the book:

Put another way, stocks protect against deep risk, but exacerbate shallow risk.

The four main causes of deep risk according to Bernstein are hyperinflation, prolonged deflation, devastation (wars or geopolitical disasters) or government confiscation of assets.

These deep risks are all completely out of your control.

Bernstein surgically dissects each deep risk in the book and shows that even though the there is a small probability of these events occurring, stocks are still your best bet to protect and grow your wealth should they transpire.

These risks can also be separated by your time horizon:

Capital managed for near-term liabilities should be guided by shallow risk, while capital managed for very long-term liabilities should be guided by deep risk.

This means if you plan on spending your money in the near-term, you need to worry about periodic losses in stocks since it can take a few years to make your money back.

But if you have a long time horizon, shallow risk in the form of short-term losses shouldn’t be your main worry.

If you have decades to invest before spending down your portfolio, your bigger risk is missing out on the long-term growth from the stock market.

A huge mistake many investors make is confusing their time horizon when some short-term event shakes their confidence. Making short-term decisions with long-term capital can be a recipe for disaster.

Here’s Bernstein on buying high and selling low:

Mistiming the market is probably the most frequent and severe form of permanent capital loss.

True financial risk should be measured in both magnitude and in duration, and the routine buy high/sell low behavior of the average investor thus constitutes a severe form of risk which is avoided by the disciplined one.

Basically you can be your own worst enemy and your actions at the extremes in the markets usually cause the most pain.

As he does in his previous books, Bernstein takes the time to distinguish the between older and younger investors when it comes to the riskiness of your portfolio:

The moral of this exercise is that older savers, with few working years/human capital remaining, will have extreme emotional difficulty maintaining their investment strategy when confronted with the face of potential deep risk; in this case, steering their portfolio by the shallow risk lighthouse and holding a higher percentage of fixed income assets would seem to be the most prudent policy.

Andon the other end of the spectrum:

Contrariwise, younger investors should navigate by the deep-risk lighthouse. After all, their best case scenario deploys their investment capital at low prices – assuming they keep their jobs through the hard times.

Trying to define a term such as risk tolerance is a nightmare for financial advisors and individual investors alike.

Bernstein’s simplification of risk into shallow and deep pools is by far one of the best definitions I have come across.

Making your portfolio decisions according to these two risks puts your entire investment plan into the correct perspective and can help avoid the devastating behaviorial mistakes that can detract from wealth accumulation.

Source:

Deep Risk: How History Informs Portfolio Design

Further Reading:

Lessons From William Bernstein

William Bernstein on Diversification

Copyright © A Wealth of Common Sense